How do insurance companies negotiate settlements? Understanding this process can save time and simplify the often-confusing world of insurance claims. When a claim is made, insurance companies must decide if the policy covers the loss and if the amount requested is accurate. If these factors are unclear, insurers may negotiate to find a middle ground:

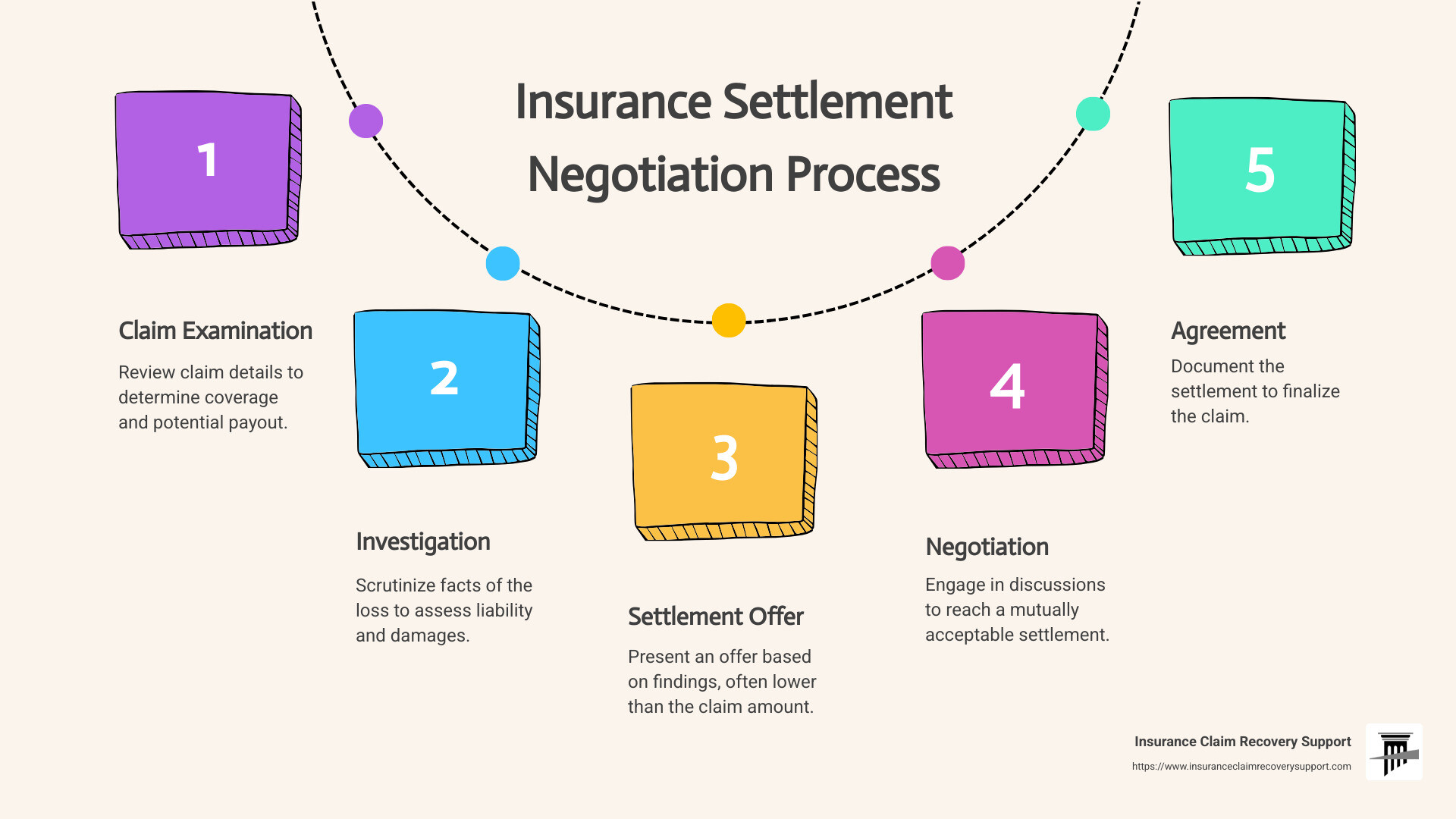

- Initial Claim Examination: Review claim details to determine coverage and potential payout.

- Investigation: Scrutinize facts of the loss to assess liability and damages.

- Settlement Offer: Present an offer based on findings, potentially lower than the claim amount.

- Negotiation: Engage in back-and-forth discussions to reach a mutually acceptable settlement.

- Agreement: Document the settlement to finalize the claim.

Navigating through these stages is vital for anyone involved in an insurance claim, helping ensure you receive what you’re entitled to without unnecessary delays.

I’m Scott Friedson, CEO of Insurance Claim Recovery Support, with experience in how do insurance companies negotiate settlements. Having managed over $250 million in large loss claims, my goal is to guide commercial property and multifamily real estate owners through the insurance maze for a fair settlement.

How do insurance companies negotiate settlements vocabulary:

– Texas insurance claims

– how do insurance companies settle personal injury claims

– how to negotiate a settlement with an insurance claims adjuster

Understanding Insurance Settlements

Insurance settlements can seem complex, but they’re all about three main ideas: risk management, policy limits, and fair evaluation.

Risk Management

Insurance companies are in the business of managing risk. They collect premiums from policyholders to cover potential losses. When you file a claim, the insurer evaluates the risk involved. They want to ensure that the amount they pay out is balanced by the premiums collected over time. This is why they carefully assess each claim before deciding on a settlement.

Policy Limits

Every insurance policy has limits. These limits define the maximum amount the insurer will pay for a covered loss. If your claim exceeds these limits, you might not receive the full amount you’re hoping for. It’s important to understand your policy limits before you file a claim. This knowledge helps you set realistic expectations for your settlement.

Fair Evaluation

A fair evaluation is crucial for both the insurer and the policyholder. Insurers must assess each claim accurately to decide if the loss is covered and if the requested amount is justified. This involves investigating the details of the incident and reviewing all evidence. If there’s room for debate, negotiations might be necessary to agree on a fair settlement.

In summary, insurance settlements revolve around balancing risk, adhering to policy limits, and ensuring fair evaluations. Understanding these elements can help you steer the settlement process more effectively and increase your chances of receiving a fair payout.

How Do Insurance Companies Negotiate Settlements?

When it comes to understanding how insurance companies negotiate settlements, it’s important to grasp their commercial motivations and the process they follow.

Commercial Motivations

Insurance companies are businesses, and like any business, they aim to maximize profits. This means they try to minimize the amount they pay out in claims. By doing so, they protect their bottom line. When negotiating settlements, insurers balance between paying claims and keeping their expenses low. This is why they often start with lower settlement offers to see if claimants will accept less.

Settlement Negotiations

The negotiation process begins after a claim is filed. Once the insurance company receives a claim, they assess it to determine if the policy covers the loss and whether the amount requested is reasonable. If there’s any uncertainty, they might offer a settlement that’s less than the claimed amount. This is a strategic move to protect their interests while still resolving the claim.

Negotiations often involve a back-and-forth exchange. The claimant might counter the initial offer with a higher demand. This can lead to several rounds of negotiation, each party presenting evidence to support their position. The goal is to reach a mutually agreeable settlement without going to court.

Claim Evaluation

During claim evaluation, insurers scrutinize every detail. They examine the policy terms, the circumstances of the loss, and any supporting evidence. This helps them decide if the claim is valid and how much they should pay. Insurers are obligated to perform this evaluation in good faith, but they may still engage in tactics to reduce the payout.

For example, they might question the severity of the damages or the claimant’s account of the incident. This is why it’s crucial for claimants to provide thorough documentation and evidence to support their claims.

By understanding the motivations and processes behind settlement negotiations, policyholders can better steer the system and advocate for a fair outcome.

Tactics Used by Insurance Companies

When dealing with insurance claims, companies often employ various tactics to protect their financial interests. Understanding these strategies can help you better steer the settlement process.

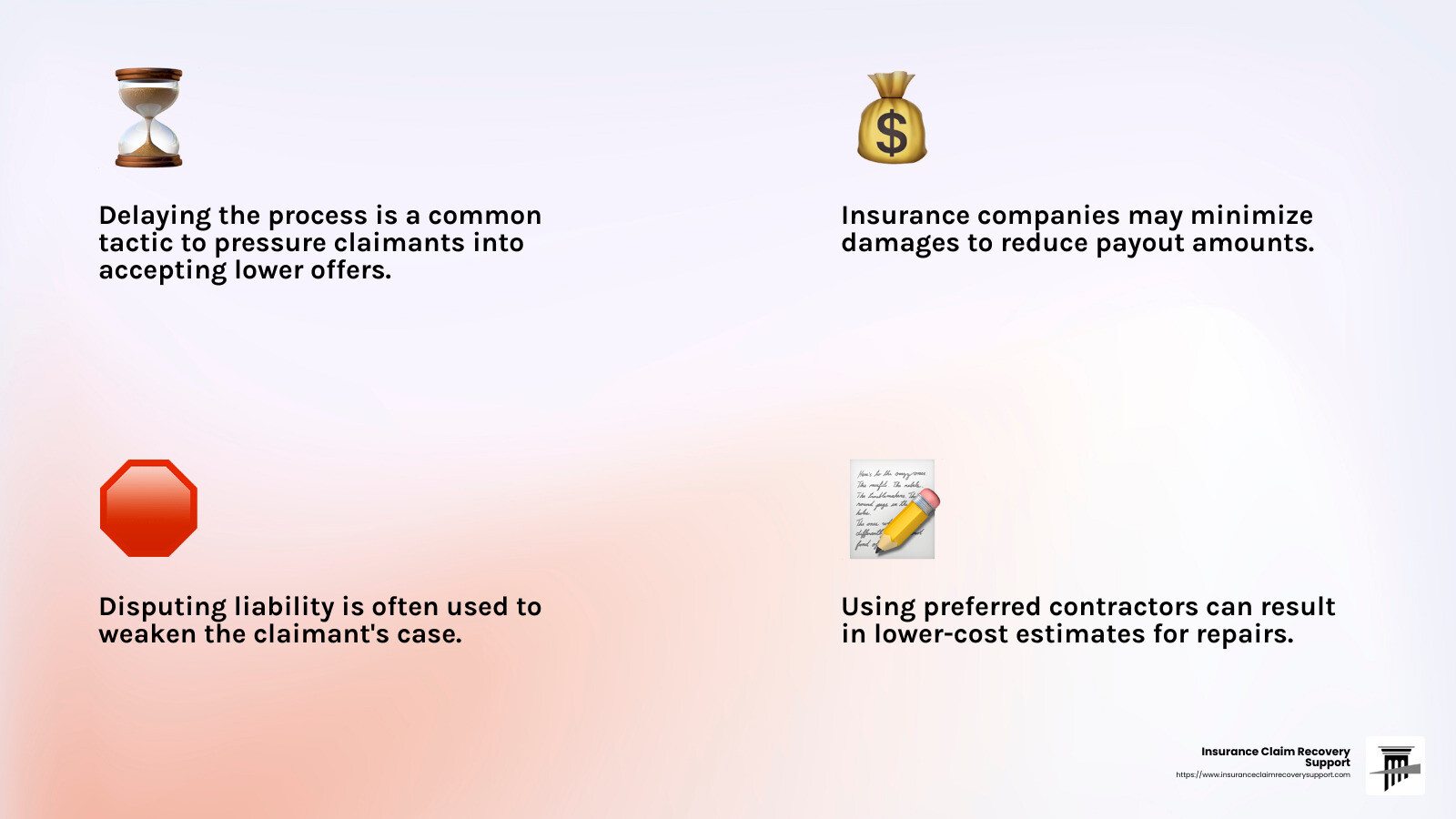

Minimizing Damages

One common tactic is to minimize the extent of damages claimed. Insurers might argue that medical treatments are unnecessary or overly expensive, or that property damage is less severe than reported. They often insist on using their preferred contractors for repairs, who may provide lower-cost estimates. This approach can significantly reduce the payout amount.

Example: After a car accident, an insurer might claim that your medical expenses are not directly related to the accident, suggesting alternative causes for your injuries. This can lead to a lower settlement offer.

Delaying the Process

Insurance companies might also delay the settlement process. By dragging out negotiations, they hope claimants will become anxious or financially strained, pressuring them to accept a lower offer. Delays can also risk the claimant missing the statute of limitations for legal action, further limiting their options.

Fact: Delays are a known strategy to encourage quick, low-value settlements.

Disputing Liability

Insurers frequently dispute liability to reduce claim payouts. They may argue that their policyholder is not at fault or that the claimant’s actions contributed to their own damages. By casting doubt on liability, insurers aim to weaken the claimant’s position.

Case Study: In a slip-and-fall incident, an insurer might argue that the claimant was wearing inappropriate footwear, thus sharing responsibility for the fall. This can lead to a reduced settlement offer.

These tactics highlight the importance of being prepared and informed when negotiating with insurance companies. Knowing how they operate can empower you to advocate for a fair settlement.

Tips for Successful Settlement Negotiation

Navigating insurance settlements can be tricky. But with the right strategies, you can increase your chances of getting a fair deal. Here are some essential tips:

Initiate Your Claim Early

Time is of the essence when it comes to insurance claims. Starting your claim as soon as possible helps preserve crucial evidence that might otherwise disappear. This is especially important in car accident cases where witness statements and accident scene details can fade quickly.

Fact: Evidence such as skid marks or eyewitness accounts can be pivotal in proving your claim. Initiating early helps secure this information.

Never Admit Fault

When discussing your claim, especially with insurance adjusters, never admit fault. It’s not your job to determine who was at fault; that’s for the professionals to sort out. Even if you think you might be partially responsible, saying so can harm your case.

Quote: “Let your lawyer handle questions of fault,” advise experts from Tittle & Perlmuter.

Know the Value of Your Claim

Understanding the rough value of your claim is crucial. Without this knowledge, you might accept a lowball offer. Research and, if necessary, consult with a professional to get a clear picture of what your claim is worth.

Example: Use resources like valuation guides to assess the value of your vehicle if it’s involved in an accident.

Be Patient

Insurance companies often start negotiations with low offers. Patience is key. Don’t rush to accept the first offer. Insurers usually have room to negotiate, and your patience can lead to a better settlement.

Tip: Reject initial low offers and be prepared for a back-and-forth negotiation process.

By following these tips, you can better position yourself in the settlement negotiation process. Being informed and prepared can make a significant difference in the outcome of your claim.

Frequently Asked Questions about Insurance Settlements

How to negotiate settlement with insurance company?

Negotiating a settlement with an insurance company can feel like a chess game. But understanding the basics can make it less daunting.

Start with a Demand Letter: This is your opening move. A demand letter outlines your claim, including the events leading up to the incident, the damages you’ve suffered, and the compensation you’re seeking. It’s crucial to be clear and detailed.

Counteroffer with Confidence: Expect the insurance company to respond with a lower offer. This is a common tactic to see if you know the worth of your claim. Don’t be discouraged. Make a counteroffer that reflects your research and the evidence you’ve gathered.

Stay Firm but Flexible: While it’s important to know your bottom line, be open to negotiation. If the adjuster provides new information that affects your claim, be willing to adjust your expectations.

How long does it take for insurance companies to negotiate a settlement?

The timeline for negotiating a settlement varies. It depends on the complexity of the claim and the willingness of both parties to reach an agreement.

Patience is Key: On average, settlements can take anywhere from a few weeks to several months. Simple claims with clear evidence might resolve quickly, while more complex cases could drag on.

Factors Affecting Timeline:

– Investigation: The insurance company needs time to investigate the claim thoroughly. This includes verifying evidence and assessing damages.

– Negotiation Rounds: Each counteroffer and negotiation round adds to the timeline.

– External Factors: High volumes of claims, like after a natural disaster, can delay the process.

Do insurance companies prefer to settle?

Insurance companies generally prefer to settle claims out of court. Here’s why:

Avoiding Lawsuits: Going to court is expensive and time-consuming for both parties. Insurance companies aim to avoid these costs by settling claims amicably.

Quick Settlements: A speedy settlement is often in the best interest of the insurer. It saves time, reduces legal fees, and minimizes the risk of a larger payout if the case goes to trial.

Commercial Motivation: Insurers want to maintain their reputation and customer satisfaction. Settling quickly and fairly can help achieve this goal.

In summary, understanding how insurance companies negotiate settlements can empower you to steer the process with confidence. Whether it’s crafting a compelling demand letter, timing your patience, or leveraging the insurer’s preference for quick resolutions, these insights can guide you through the settlement journey.

Conclusion

Navigating insurance settlements can be overwhelming. But with the right support, it doesn’t have to be. At Insurance Claim Recovery Support, we focus on maximizing settlements for policyholders, ensuring you receive what you deserve.

Our Expertise

We specialize in property damage claims, including those from fire, hurricanes, and floods. Our team is dedicated to advocating for you, not the insurance company. We understand the tactics insurers use to minimize payouts and delay the process. Our knowledge and experience allow us to counter these strategies effectively.

Policyholder Advocacy

We stand firmly on your side. You’re not just another claim number to us. You’re a valued client, and we are committed to guiding you through the insurance claim process. Our goal is to secure the maximum settlement possible, allowing you to rebuild and move forward after a loss.

Your Partner in Recovery

Whether you’re in Austin, Dallas, or anywhere else in Texas, we’re here to help. Our local presence and understanding of the Texas insurance landscape make us a valuable partner in your recovery journey.

Don’t face the insurance companies alone. Let us be your advocate and partner in achieving the settlement you deserve. Reach out to us for a consultation and take the first step towards restoring your property and peace of mind.